Typical processing

Pay a percentage on card volume

- Interchange, network fees, and processor markup on every sale

- Monthly fees and add-ons vary by provider

- Customers often see one posted price

- Statement line items can be hard to audit

Croft dual pricing lets customers choose cash or card while your card price reflects acceptance costs. Compliant setup, clear signage, and a Croft consultant from quote to go-live.

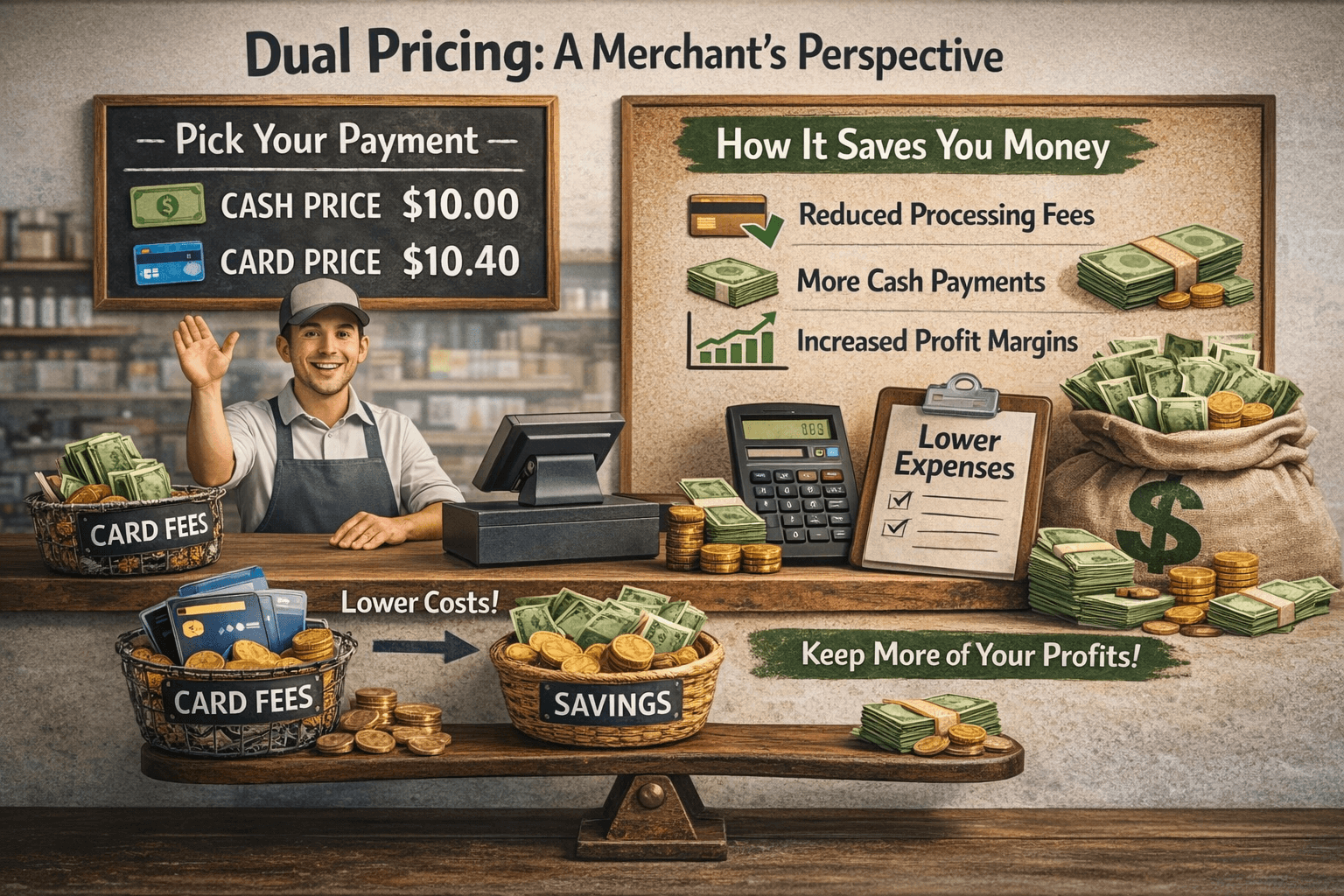

Traditional processing charges a percentage on card volume. That cost is real, but it is often invisible to customers and painful for owners who already priced their goods to make a living.

Dual pricing posts a cash price and a card price before payment. Card payers see what card acceptance costs. Cash payers get the lower posted amount. You stop subsidizing every card sale out of hidden margin.

Simple structure. Compliance handled with Croft support.

You set the cash price you want to keep. The card price is built from that number so card acceptance costs are reflected in what card payers see.

Menus, signage, and registers show cash and card pricing before the customer pays. No surprise fees added at the last second.

Croft configures your POS, trains your staff, and documents disclosures so the program follows card network and state rules.

They see both prices before they pay. Cash customers get the lower posted amount. Card customers pay the card price that matches your compliant program. No awkward fee added at the end of the transaction.

Illustrative math only. Your Croft rep builds the real proposal from your statement and volume.

Enter a cash-side price you price from (not necessarily the exact sticker line). See example posted card and cash for the same ticket, then compare offset processing costs + $35/mo program service to what you pay today.

Example ticket prices

Posted card is $1.00 above the cash basis you entered (4% on that basis). Cash in this demo matches your basis; your live menu or register lines may differ after rounding and program rules.

Monthly snapshot

You pay today (est.)

$1,462.50

3.25% × volume

With Croft

Offset card costs

+ $35.00/mo

Illustrative savings vs today

About $1,427.50/mo less

Illustrative only. Not tax or legal advice. Card-brand rules and disclosures apply; your live program depends on equipment and underwriting.

Every business is different. This is how the structures compare at a glance.

Typical processing

Croft dual pricing

Want pass-through pricing instead? Compare interchange plus or read how Croft pricing works.

When every card sale carries a percentage fee, margin disappears quietly. Dual pricing moves that cost into a posted card price customers can see upfront.

Restaurants, retail, salons, and service businesses use dual pricing when cash and card mix matters and transparency at the register builds trust.

Dual pricing shows two prices for the same item. Surcharging adds a fee on top of one price. Rules differ. Croft helps you run the model that fits your state and setup.

Your rep walks through compliance, equipment, and rollout. Same team from quote through go-live.

Enroll in dual pricing and Croft can place modern Clover terminals with compliant cash and card pricing already configured.

Hardware offers require approval. Models and terms vary by program and volume.

Straight answers before you change how you price at the register.

Dual pricing means posting two prices for the same product or service: a lower cash price and a card price that reflects the cost of card acceptance. Customers choose how they pay. The goal is to recover card costs without hiding fees at checkout.

Yes, when implemented correctly under card network and state rules. Croft helps with compliant menus, signage, register setup, and receipt language so your program is disclosed the right way.

Surcharging adds a fee on top of a single posted price, usually on credit cards only. Dual pricing shows two separate prices upfront. The right model depends on your business type, state, and how you sell.

It is the flat monthly service tied to your dual pricing enrollment and ongoing program support. Your Croft rep confirms exact inclusions for your account before you sign.

Most pushback comes from confusion, not from two clear prices. When signage, menus, and staff messaging match what the register shows, customers understand they are choosing how to pay.

Yes. If dual pricing is not the right long-term fit, talk with Croft about interchange plus, flat rate, or other structures.

Still deciding? Talk to Croft or start with a free statement review.

We will review your volume, walk through compliance, and show you posted pricing examples. No obligation.